Are Personal Injury Settlements Taxable in California?: In-Depth Guideline

- Generally Not Taxable: Personal injury settlements are typically non-taxable for physical injuries, medical costs, and pain and suffering.

- Taxable Components: Punitive damages, interest, and lost wages are always taxable.

- Physical Injury Link: Emotional distress is only tax-free if directly tied to a physical injury.

- Documentation Matters: The settlement agreement should clearly specify the allocation of damages to minimize taxes.

- Seek Professional Help: Consult with a personal injury attorney and a tax advisor to properly handle the tax implications of your settlement.

The disbursement of personal injury settlements provides relief to people. However, it also brings a crucial query: “Are personal injury settlements taxable in California? Do I have to pay taxes on my personal injury and lost wages settlement?”

Generally, the settlement amount for medical bills and pain and suffering is linked to injuries. However, you must pay taxes on punitive damages and interest from your settlement. The amount received for lost wages is also taxable according to the IRS, as it compensates for your taxable wages.

Are Personal Injury Settlements Taxable in California?

California follows the federal rule of taxation on personal injury settlements. So, generally, it’s not taxable. The court considers it a form of compensation for a loss, not a source of income. The IRS and the state of California follow a key principle: damages received on account of a personal physical injury or physical sickness are excluded from gross income.

So, the majority of a typical personal injury award, particularly for core damages, is tax-free.

Personal Injury Settlements that are Not Taxable:

- Medical Expenses: Compensation for past, present, and future medical bills, including hospital stays, surgeries, physical therapy, and prescription medications.

- Pain and Suffering: Money awarded for physical pain, emotional distress, and mental anguish if it is a direct result of the injury.

- Property Damage: Compensation for the damaged or lost property, as long as the amount does not exceed the property’s basis (original value).

- Loss of Consortium: Damages awarded to a spouse or family member for the loss of companionship and support due to the victim’s physical injury.

Understanding State and Federal Taxation

The federal government (through the IRS) and the state of California have specific taxation rules for personal injury claims. According to Internal Revenue Code Section 104, damages received on account of “personal physical injuries or physical sickness” are excluded from gross income.

Federal Taxation on Personal Injury Settlements:

According to the IRS Publication 525, all income is taxable unless specifically excluded by another section of the tax code. IRC Section 104 excludes damages related to personal physical injuries and physical sickness from the taxable section.

So, if you receive a settlement for medical expenses, pain and suffering, or other damages directly stemming from a physical injury, that portion is typically not taxable.

Table 1: Federal Taxability of Personal Injury Settlement Components:

| Component of Settlement | Is it Taxable? | IRS Rationale |

| Damages for Physical Injuries (e.g., medical costs) | No | Covered by IRC Section 104; directly compensates for physical harm. |

| Punitive Damages | Yes | Punishes the wrongdoer; taxable income. |

| Damages for Emotional Distress (not from physical injury) | Yes | Not considered a physical injury; treated as income unless directly tied to a physical injury. |

| Lost Wages/Lost Profits | Yes | Considered a substitute for income, which would have been taxable if earned. |

| Interest on the Settlement | Yes | Classified as interest income, a separate category of taxable income. |

California State Tax Considerations:

California generally aligns with the federal government on the taxability of personal injury settlements. Damages for physical injuries, medical expenses, and pain and suffering are typically non-taxable at the state level. However, California law also specifies that punitive damages and interest on an award are taxable.

Tax Filing Timeline for Personal Injury Settlements:

Since the IRS and California State Law are strict with taxation policy, always follow their tax filing deadline. Otherwise, your settlement may be subject to a penalty, along with the tax.

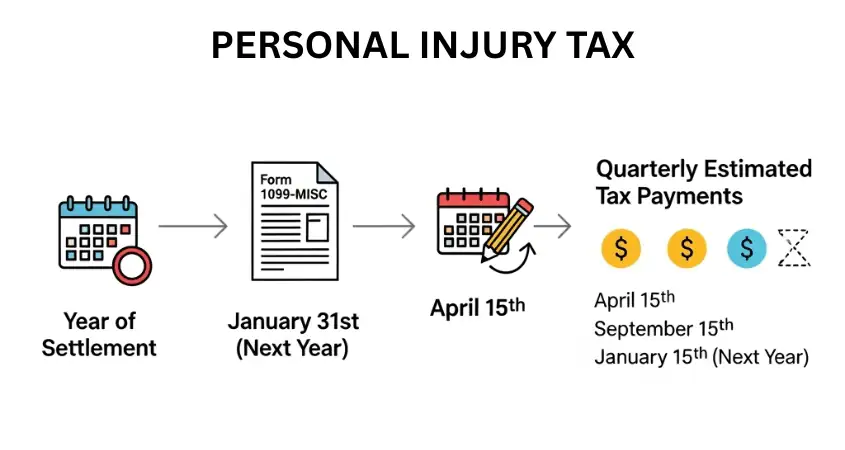

Year of Receipt: Report the taxable portion of a settlement on your tax return for the year in which you actually receive the funds.

- Form 1099-MISC: If your settlement includes taxable components (e.g., lost wages, punitive damages, interest) over $600, the payer will issue you a Form 1099-MISC by January 31st of the following year.

- Filing Deadlines: The standard tax filing deadlines for both federal (IRS) and state (FTB) returns are April 15th of the year after you receive the settlement.

- Non-Taxable Portions: While you don’t owe tax on them, report the total settlement. Use a statement on the tax return to clarify which portions are non-taxable and why, to prevent an audit.

- Estimated Taxes: If the taxable portion of your settlement is large, choose to pay quarterly estimated taxes to avoid underpayment penalties. A tax professional will determine if this applies.

- Documentation is Key: Keep all settlement documents, including the agreement and any 1099 forms, to support your tax filings and in case of an audit.

Do You Have to Pay Taxes on Damages for Past and Future Medical Expenses?

You don’t have to pay taxes on damages for past and future medical expenses. It includes hospital stays, surgeries, physical therapy, and prescription medications. These funds compensate you for costs incurred due to bodily injury.

Medical Expenses as Tax-Free Damages

Did you deduct medical expenses on a prior year’s tax return? You are then reimbursed for those same expenses in a settlement. If so, you must report the reimbursement as income in the year you receive the settlement. It prevents you from obtaining a tax deduction for a cost you ultimately did not bear.

Do You Have to Pay Taxes on Damages for Past and Future Lost Wages?

Damages for lost wages or loss of earning capacity are considered taxable income. It’s because the settlement for lost wages serves as a replacement for your potential income. Wages are taxable. So, the money you receive to replace them is also taxable.

Lost Wages and Their Tax Implications:

Allocate the settlement in various sectors in your agreement. If your lost wages are not specified, the IRS may tax them. A skilled attorney will structure the settlement in a way that accurately reflects the non-taxable damages. It will separate non-taxable incomes from taxable damages, such as lost wages and other similar losses.

Do You Have to Pay Taxes on Damages for Property Losses?

In most cases, compensation for property damage is non-taxable. However, the amount received must not exceed your adjusted basis in the property. For example, if your car was worth $20,000 and you received $20,000 in a settlement for it, you don’t pay taxes.

Property Loss Damages: Taxable or Not?

The taxability of property loss damages depends on two points:

- Amount below your evaluated property damage (Non-taxable)

- Amount above the evaluated property loss (Taxable)

At times, the settlement amount exceeds the property’s basis. So, it will be a taxable capital gain. If you receive a settlement for a property that is less than or equal to its basis, you generally do not need to report it as income.

Do You Have to Pay Taxes on Damages for Pain and Suffering?

Damages for pain and suffering, emotional distress, and similar non-economic damages are non-taxable. However, it must be directly linked to a physical injury.

Pain and Suffering: Typically Non-Taxable:

Emotional distress or pain and suffering won’t be taxable if it is a direct result of a physical injury. For instance, you suffer anxiety and depression because of a car accident that caused you physical injuries. So, the damages for that emotional distress are not taxable. But compensation for defamation would likely be taxable.

Do You Have to Pay Taxes on Punitive Damages or Interest?

Yes, punitive damages and interest on a settlement are taxable under both federal and California state law. These are two of the most significant exceptions to the general rule that settlements are tax-free.

Punitive Damages and Their Tax Status:

Punitive damages punish the defendant for their malicious or particularly egregious conduct. It is not meant to compensate the victim. Since punitive damages are not compensation for a physical injury, the IRS and the FTB consider them taxable income. It applies even if they are part of a settlement for a bodily injury.

Interest on Settlements: Is It Taxable?

Any interest that accrues on your settlement or award is taxable interest income. This can happen if there is a delay between the court award and the actual payment. The IRS and California treat this interest as a separate category of income.

How Do You Figure Out How Much of an Award Is Allocated for Each Category of Damages?

The language in the settlement agreement is key. To avoid tax issues, a settlement agreement should clearly and specifically allocate the funds among the different types of damages (e.g., medical expenses, lost wages, pain and suffering, punitive damages).

Breakdown of Settlement Allocations:

Without a specific breakdown, the IRS and the FTB have the right to look at the original complaint. Also, they decide how the settlement should be taxed.

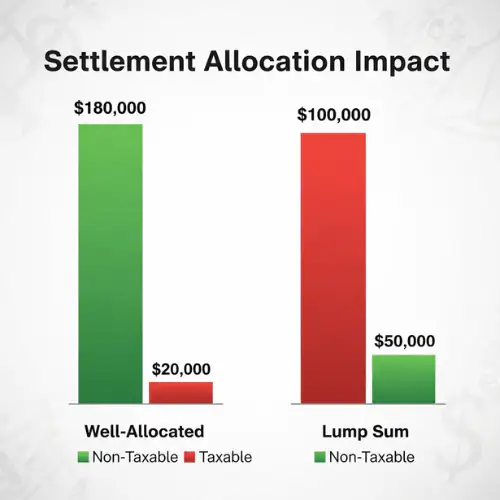

| Settlement Allocation Strategy | Tax Outcome for Plaintiff | Rationale |

| Clearly Allocated Settlement | Minimizes tax liability. | IRS respects a good-faith allocation that reflects the true nature of the claim. |

| Undifferentiated Lump Sum | High risk of being taxed on a larger portion. | The IRS will make its own allocation based on the original complaint. |

| Over-Allocated to Non-Taxable Damages | High risk of an IRS audit. | If the allocation is unrealistic, the IRS can reallocate the funds for tax purposes. |

| Specific Allocation Example: $100,000 | Only the $20,000 for lost wages is taxable. | $80,000 for Medical/Pain & Suffering (Non-Taxable) + $20,000 for Lost Wages (Taxable). |

| General Settlement Example: $100,000 | A larger, unspecified amount may be subject to taxation. | The IRS may assume a pro-rata allocation, potentially taxing a larger portion than necessary. |

Settlement Parts That Are Not Generally Taxable in California:

In California, similar to federal law, certain damages are considered non-taxable. It includes damages for physical injury and emotional distress.

Physical Injury Damages:

Any compensation for a physical injury or physical sickness is non-taxable. This includes:

- Medical bills: Past and future medical costs.

- Pain and Suffering: Compensation for physical and mental pain, disfigurement, and loss of enjoyment of life. It must arise from a physical injury.

- Loss of consortium: Damages awarded to a spouse for loss of companionship or support due to the physical injury of their partner.

Emotional Distress Damages:

As previously mentioned, if emotional distress damages are a direct result of a physical injury, they are considered non-taxable.

Components of Non-Taxable Settlements:

| Component of Settlement | Key Consideration |

| Compensatory Damages | Must be for “personal physical injuries or physical sickness” |

| Emotional Distress | Must be directly related to a physical injury |

| Lost Wages | Generally taxable, but can be non-taxable in rare cases where they are not replacing income but rather compensating for a loss directly tied to a physical injury. |

| Property Damage | Non-taxable if the settlement amount does not exceed the property’s adjusted basis. |

Components of Personal Injury Settlements That May Be Taxable:

The taxable part of your compensation includes lost wages, profits, and interest on awards. Additionally, punitive damages are considered taxable under both IRS and California insurance law.

Taxable Damages in Personal Injury Settlements:

In California, the following types of damages are generally taxable:

- Lost Wages and Lost Profits: A substitute for income.

- Punitive Damages: To punish the wrongdoer, not to compensate for injury.

- Interest on the Award: Classified as interest income.

- Damages from Non-Physical Injuries: For example, emotional distress from defamation or breach of contract.

- Medical Expenses Previously Deducted: Amounts reimbursed for medical costs for which you previously took a tax deduction.

IRS Guidelines on Settlement Taxability:

The IRS has an unequivocal stance: the taxability of a settlement is determined by the “origin of the claim.” In other words, what was the settlement intended to replace? If it were to replace taxable income, such as wages, it would be taxable. If it were to replace a loss from a physical injury, it is not taxable.

What Lawsuit Settlement is Taxable?

Beyond personal injury, many types of lawsuit settlements are fully or partially taxable. These include:

- Employment disputes: Back pay, front pay, and other damages for wrongful termination, harassment, or discrimination are generally taxable.

- Breach of Contract: Damages resulting from a breach of contract are typically taxable.

- Defamation: Damages from a defamation lawsuit are considered taxable.

Lawsuit Settlement Types and Their Tax Status:

Any settlement that does not arise from a physical injury or physical sickness is likely to be taxable. Therefore, the original legal complaint must state that the claim is for “personal physical injuries” to avoid taxation.

What Lawsuit Settlement is Not Taxable?

A lawsuit settlement is not taxable for damages of personal physical injury or physical sickness. This includes compensatory damages for:

- Medical expenses (past and future)

- Physical pain and suffering

- Loss of consortium (for a spouse)

Attorney Contingency Fees and Taxation:

In most personal injury cases, the attorney’s fees are paid from the settlement before the client receives their share. A significant 2004 Supreme Court case, Commissioner v. Banks, ruled that attorney fees paid from a taxable settlement are considered income to the client. So, generally, it’s not tax-deductible.

Impact of Attorney Fees on Your Settlement:

The impact of attorney fees on your settlement depends on different factors. First, is it a contingency fee or an upfront one? Additionally, what is the attorney’s share of the personal injury payout?

Primarily, personal injury attorneys receive 20% to 40% of your settlement. So, work with a knowledgeable attorney to understand the tax implications of your fees.

Working With the Right Professionals:

You should work with an experienced personal injury lawyer to know the deductible and non-deductible parts of your compensation. Experienced lawyers at Ledger Law Firm will clarify the matter and ensure that the minimum tax is deducted.

The Importance of Legal and Tax Advisors:

Always work with an experienced personal injury attorney and a tax professional. An attorney will negotiate a settlement that is structured to minimize your tax burden. On the other hand, a tax advisor will understand your specific obligations and accurately file your return.

FAQs About California Taxable Personal Injury Settlements:

Is Compensation for Physical Injuries Taxable?

No, compensation for physical injuries, including medical costs, is generally not taxable.

Are Pain and Suffering Damages Taxable in California?

No, as long as pain and suffering are directly linked to a physical injury, they are not taxable in California.

Do I Have to Pay Taxes on Lost Wages in a Personal Injury Settlement?

Yes, damages for lost wages are considered taxable income and are subject to both federal and state taxes.

Is Interest on a CA Personal Injury Settlement Taxable?

Yes, any interest earned on a personal injury settlement is considered taxable income.

Are Punitive Damages in Personal Injury Settlements Taxable?

Yes, punitive damages are always taxable, even if they are part of a personal injury settlement.

Do I Have to Report My Settlement When I File Taxes?

You must report your taxable settlement portion. For non-taxable settlements, report them to the IRS to explain the source of the funds and avoid potential audits.

How Do I Determine the Taxable Portion of My Personal Injury Settlement?

Your attorney and a tax professional can help you. The settlement agreement itself should clearly specify the allocation of damages, which will serve as a guide.

What Happens If I Don’t Report a Personal Injury Settlement to the IRS?

If a portion of your settlement is taxable and you fail to report it, you could face penalties, interest charges, and a tax audit.

Talk to an Experienced Personal Injury Attorney:

The tax implications of a personal injury settlement are highly complex. So, hire a skilled personal injury attorney to maximize your payout. They will do everything from gathering evidence to negotiating with insurance companies. Also, they will structure your settlement in a tax-advantageous way.

Emery Brett Ledger brings more than 27 years of experience to personal injury law. He founded & led The Ledger Law Firm in securing over $100 million in compensation for clients with life-altering injuries & complex claims. Licensed in California, Texas, & Washington, Emery earned his law degree from Pepperdine University School of Law. His practice areas include car & truck accidents, wrongful death, catastrophic injuries, maritime claims, & mass tort litigation. He has been recognized by The National Trial Lawyers’ Top 100, Mass Tort Trial Lawyers Top 25, and America’s Top 100 Personal Injury Attorneys. Emery also received the 2025 Elite Lawyer Award & holds a perfect 10.0 Avvo rating with Platinum Client Champion status. His legal work has been featured on CNN, Forbes, NBC, & ABC.

Free Case Evaluation

Recent Posts

- How to Sue a Restaurant for Negligence: Your Guide to Restaurant Negligence Cases and Compensation

- Can You Sue a Restaurant for Food Poisoning? Your Legal Rights, Evidence, and Compensation Explained

- What Is Considered a Serious Car Accident? Understanding Serious Injuries, Legal Rights, and Compensation

- Can a Lawsuit Be Reopened After Settlement? When You May Be Able to Reopen a Settled Case

- Can You Sue a Car Company for Airbags Not Deploying? Legal Guide for Injuries Caused by Defective Air Bags

Emery Brett Ledger brings more than 27 years of experience to personal injury law. He founded & led The Ledger Law Firm in securing over $100 million in compensation for clients with life-altering injuries & complex claims. Licensed in California, Texas, & Washington, Emery earned his law degree from Pepperdine University School of Law. His practice areas include car & truck accidents, wrongful death, catastrophic injuries, maritime claims, & mass tort litigation. He has been recognized by The National Trial Lawyers’ Top 100, Mass Tort Trial Lawyers Top 25, and America’s Top 100 Personal Injury Attorneys. Emery also received the 2025 Elite Lawyer Award & holds a perfect 10.0 Avvo rating with Platinum Client Champion status. His legal work has been featured on CNN, Forbes, NBC, & ABC.